If you are in your 20s right now and you feel like money is something that just never stays in your hands, this post is for you. Whether you just got your first job, you are freelancing, you are building a side hustle, or you are still figuring things out, the truth is this: your 20s are the best time to get your money right.

Not because you have a lot of it. But because time is on your side.

Let’s get into it.

Why Your 20s Are the Most Important Money Years of Your Life

Most people think you only need to start thinking about money when you are older. When you have a “real job.” When you earn more. When life settles down.

That is a trap.

The habits you build in your 20s will follow you for decades. The way you spend, save, and think about money right now is literally shaping the financial life you will have at 35, 45, and beyond.

Here is something that will blow your mind: if you invest just $5,000 a year starting at age 25 and stop at age 35, you would have around $787,000 by the time you turn 65. But if you wait until 35 to start, you would need to invest $5,000 every single year for 30 years straight to end up with less, around $612,000. That is the power of starting early.

You do not need a lot of money to start. You just need to start.

Step 1: Know Where Your Money Is Actually Going

Before you can fix anything, you need to see the full picture. Most people have no idea where their money goes. They earn, spend, and wonder why there is nothing left.

The first thing to do is track your spending for one full month. Write down every single thing you spend money on. Food, transport, airtime, subscriptions, clothes, everything. Do not judge yourself. Just look.

You will probably be shocked.

Most people discover they are spending a huge chunk of their income on things they barely think about. Small daily purchases that seem harmless but add up fast.

This step is not about feeling bad. It is about getting honest. Because you cannot manage what you cannot see.

Write everything down in a notebook, a simple spreadsheet, or even the notes app on your phone. The goal is just to get clarity. Once you see where your money is going, you can make smart decisions about where it should go instead.

Step 2: Build a Budget That Actually Works for You

A budget sounds boring. But it is honestly the most powerful money tool you have.

Think of a budget as a plan. Before your money comes in, you decide where it is going. That is it. You are just giving every naira or dollar a job.

One of the most popular and beginner-friendly budget frameworks is the 50/30/20 rule.

Here is how it works:

50% of your income goes to needs. This covers rent, food, transport, phone bills, utilities. The basics.

30% goes to wants. This is entertainment, eating out, clothes, fun things. Yes, you are allowed to enjoy life.

20% goes to savings and financial goals. Emergency fund, investments, paying off debt.

If 20% feels too much right now, start with 10%. Or even 5%. The amount matters less than the habit. Getting into the rhythm of setting money aside every single time you receive income is what changes everything.

A tip that works really well: pay yourself first. The moment money comes in, move your savings out before you touch anything else. If you wait until the end of the month to save what is left, there is usually nothing left.

Step 3: Build an Emergency Fund Before Anything Else

Life happens. Your phone breaks. You get sick. Transport costs go up. Something unexpected always comes up.

Without an emergency fund, any small crisis sends you into panic mode or worse, into debt.

An emergency fund is simply money you keep aside and only touch during real emergencies. Not for a new outfit. Not because something is on sale. Real emergencies.

Start small. Your first goal is to save your first $100 or the equivalent in your currency. Then work your way up to $500. Then aim for one month of your basic expenses. Eventually, the goal is three to six months of living expenses sitting in a separate account.

Keep this money somewhere you will not easily access it. A separate savings account that is not linked to your main account works well. Out of sight, out of temptation.

Having even a small emergency fund completely changes how you feel about money. It gives you breathing room. You stop living in fear of what might go wrong because you have something to catch you.

Step 4: Deal With Debt (Especially the Expensive Kind)

Not all debt is the same. A business loan or a student loan that helps you build income is different from high-interest consumer debt.

Credit card debt and high-interest personal loans are the kind that can quietly destroy your financial future. The interest keeps growing, and before you know it you are paying back twice what you originally borrowed.

If you have high-interest debt right now, make it a priority to pay it off. There are two popular strategies:

The snowball method: Pay off your smallest debt first while making minimum payments on the rest. Once the smallest is gone, roll that payment toward the next one. This gives you quick wins and keeps you motivated.

The avalanche method: Pay off the debt with the highest interest rate first, regardless of size. This saves you more money in the long run.

Either works. The best one is the one you will actually stick to.

And going forward: try your hardest to avoid consumer debt. Do not buy things on credit that you cannot afford to pay off by the end of the month. It feels convenient in the moment but it steals from your future.

Step 5: Start Saving, Even If It Is a Small Amount

Here is a mindset shift that changes everything: saving is not something you do with what is left. Saving is something you do first.

Even if you can only save $10 or $20 a month right now, do it. Saving $20 a week adds up to over $1,000 in a year. That is not nothing. That is a real cushion.

The goal in your 20s is to build the habit. Your income will grow over time. But if you do not have the habit of saving, a bigger income will just mean bigger spending, and you will still end up with nothing.

Here are a few practical ways to save more:

Cook at home more often instead of eating out every day. This alone can save you thousands over a year.

Cancel subscriptions you forgot you had. Go through your bank statement and look for anything you are paying for monthly that you do not use.

When you want to buy something, wait 48 hours. If you still want it after two days, it is probably not an impulse. If you forgot about it, you did not actually need it.

Buy secondhand when it makes sense. Clothes, furniture, electronics. There is no shame in saving money.

Look for free or low-cost versions of things you enjoy. Entertainment, learning, fitness.

Frugal living does not mean living a miserable life. It means being intentional. It means choosing to spend your money on things that actually matter to you, not things that just feel good for five minutes.

Step 6: Understand Credit and Use It Carefully

Credit is a tool. Like any tool, it can help you or hurt you depending on how you use it.

A good credit score opens doors. It helps you get approved for loans when you need them, negotiate better rates, and sometimes even get better deals on services.

A bad credit score closes doors and costs you more money in the long run.

To build good credit in your 20s:

Pay your bills on time. This is the single biggest factor in your credit score.

Do not use all of your available credit at once. If you have a credit limit of $1,000, try not to go above $300 at any time.

Only take on credit you actually need and can manage.

Check your credit report regularly for any errors.

If you are young and do not have credit history yet, that is okay. You can start building it by getting a basic credit card or a secured card, using it for small purchases, and paying it off in full every month. Over time, your score will grow.

Step 7: Learn the Basics of Investing

Investing sounds complicated. It is not. At least not at the beginning.

Investing is simply putting your money to work so that it grows over time, even while you are sleeping.

The reason investing in your 20s is so powerful is compound interest. This is when you earn returns not just on the money you put in, but also on the returns you have already earned. Over time, this creates exponential growth.

Here is a simple example: if you invest $200 a month starting at age 25 and earn an average annual return of 7%, you could end up with well over $500,000 by retirement. If you wait until 35 to start, the same $200 a month gets you dramatically less.

Time is the secret ingredient. And you have it right now.

You do not need a lot of money to start investing. Many platforms let you begin with as little as $10 or $50 a month. The key is to start and stay consistent.

For absolute beginners, here are the basics:

Index funds are a popular starting point. They let you invest in a whole group of companies at once instead of picking individual stocks. Lower risk, lower effort, consistent long-term growth.

Retirement accounts like a Roth IRA (if you are in the US) allow your money to grow tax-free. Always take advantage of any employer retirement matching if it is available to you. That is literally free money.

Start before you feel ready. Most people wait until they understand everything before they invest. But you learn most by doing. Start small, invest in learning as you go, and build from there.

Step 8: Start Making More Money

Saving and budgeting are important. But they have a ceiling. You can only cut so much.

The real game-changer is growing your income.

Your 20s are the perfect time to start building income streams outside of your main job. Here is why: you have fewer obligations, more energy, and more time to experiment.

Some ways people in their 20s are building extra income:

Freelancing using skills you already have. Writing, design, social media management, coding, photography, data entry.

Digital products. Creating eBooks, templates, guides, Canva designs, or online courses that you sell once and earn from repeatedly.

Affiliate marketing. Recommending products you genuinely use and earning a commission when someone buys through your link.

Content. Growing an audience on social media around a topic you know and love, then monetizing it through brand deals, digital products, or coaching.

The key is to start with one thing and go deep before jumping to the next. Most people fail at building extra income because they try five things at once and stick with none.

Pick one, learn it, work it consistently for 90 days, then evaluate.

Step 9: Set Clear Financial Goals

Budgeting and saving feel pointless without a reason why.

That is why you need goals. Real, specific ones.

Not “I want to save money.” That is too vague.

Try: “I want to save $1,500 by December so I can pay for my first professional course without going into debt.”

Or: “I want to pay off this $800 debt by the end of the next three months.”

Or: “I want to have $500 saved as an emergency fund before I turn 25.”

Specific goals give your money a purpose. And when your money has a purpose, it stops disappearing.

Write your goals down. Review them every month. Adjust as things change. Celebrate small wins, because they keep you going when motivation dips.

Step 10: Invest in Yourself

This is the money tip nobody talks about enough.

The best investment you can make in your 20s is in your own skills, knowledge, and mindset.

A course that teaches you a high-income skill could return 10 times what you spent on it within a year. A book on personal finance could save you thousands in mistakes. A mentor who has already figured out what you are trying to figure out could cut your learning curve by years.

Spend money on things that grow your earning potential. Not just on things that feel good right now.

Read books on money, business, and investing. Watch YouTube videos from credible financial educators. Follow people who have the kind of financial life you want and learn from them.

Your mindset about money is the foundation everything else is built on. If you believe money is hard to get and easy to lose, that will be your reality. But if you start seeing money as something you can learn to manage, grow, and multiply, everything changes.

Here is the honest truth: knowing all of this information is one thing. Actually doing it is another.

Most people read posts like this, feel motivated for a few days, and then go back to their old habits. Not because they are lazy. But because there is a big gap between knowing and doing.

That gap is where a planner comes in.

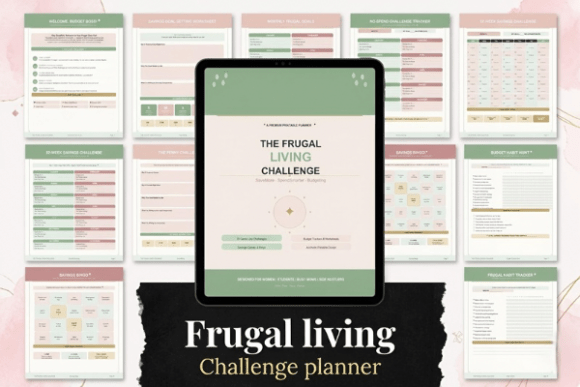

The Frugal Living Planner was put together specifically for people who are starting from scratch, people who want to stop the paycheck-to-paycheck cycle, build real savings, and live intentionally without feeling deprived.

Inside the planner, you will find:

A monthly budget tracker where you map out your income, fixed expenses, and savings goals in one clear place. No guessing, no chaos.

A spending tracker to record your daily expenses so you can finally see your habits clearly.

A savings goal tracker to keep your eyes on what you are actually working toward.

A debt payoff planner to map out your payments and watch your debt shrink month by month.

A frugal living habit checklist with simple daily and weekly actions that add up to real change over time.

It is designed to be simple. You do not need to understand complex finance to use it. You just need to open it, fill it in, and check in with it regularly.

Whether you are trying to save your first $1,000, pay off debt, or finally stop wondering where your money went, the Frugal Living Planner gives you a clear, practical system to make that happen.

This is the kind of tool that turns “I’ll start next month” into action you take today.

A Quick Recap: Your 20s Money Checklist

Here is everything covered in this post, in simple summary form:

Track your spending for one full month so you can see where your money really goes.

Build a budget using the 50/30/20 rule or any system that works for your life.

Start an emergency fund, beginning with your first $100 and building from there.

Deal with high-interest debt aggressively using the snowball or avalanche method.

Save first, not last. Move money out before you have a chance to spend it.

Build your credit slowly and responsibly by paying bills on time and avoiding unnecessary debt.

Start investing early, even with small amounts. Time and consistency matter more than the size of your investment.

Build extra income through freelancing, digital products, content creation, or affiliate marketing.

Set specific financial goals with real timelines.

Invest in yourself: courses, books, mentors, skills.

Use a system like the Frugal Living Planner to stay on track every single month.

Final Words

Your 20s are not too early to get serious about money. They are actually the perfect time.

You do not need to have it all figured out. You do not need to be earning a lot right now. You just need to start somewhere. One habit. One goal. One decision to show up for your future self.

The people who build real wealth do not have some secret that you do not have. They just started earlier, stayed consistent, and made small smart choices over and over again.

You can do that too.

Start today. Your future self will thank you.